0% read

Last updated:

PACE Act

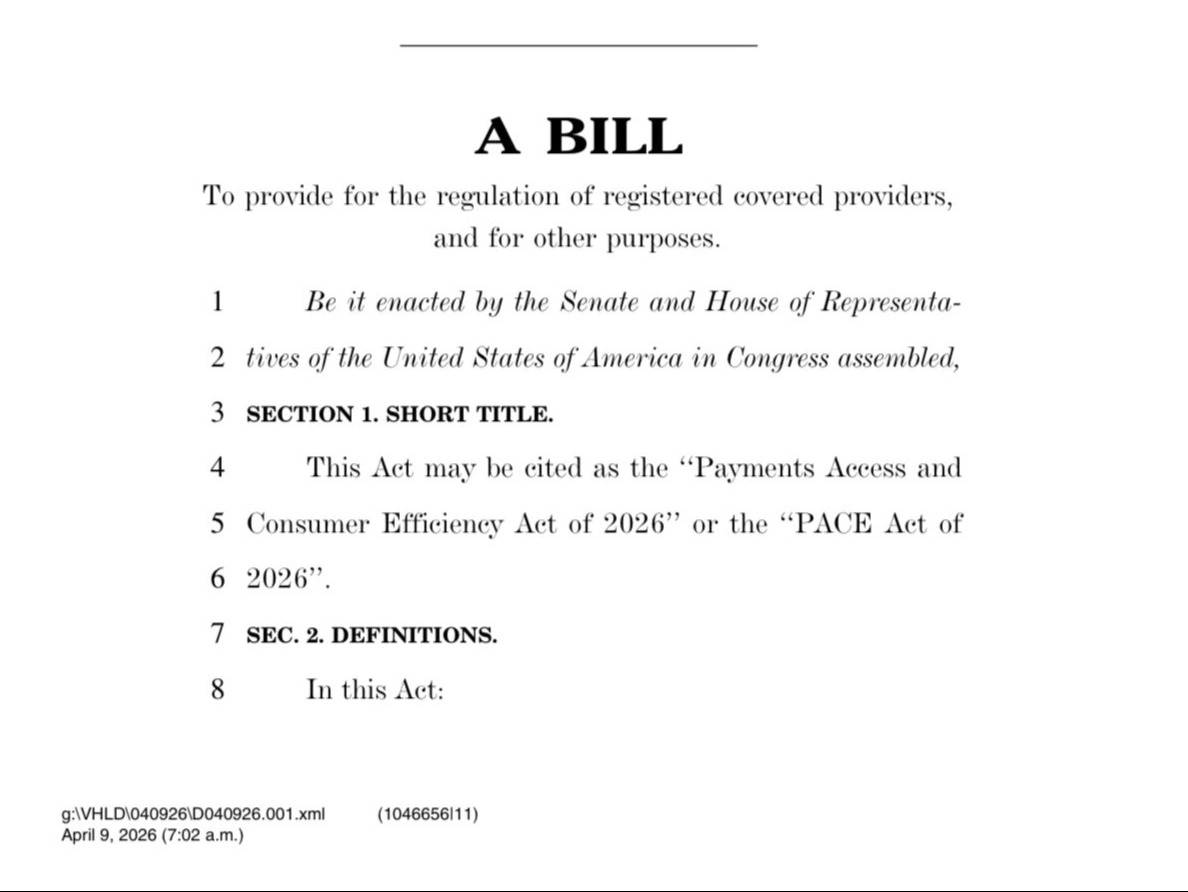

The Payments Access and Consumer Efficiency Act (PACE Act) is a bipartisan bill introduced on April 21, 2026, that proposes a new pathway for qualified nonbank payment providers to access Federal Reserve payment services. Sponsored by U.S. Representatives Young Kim (R–CA) and Sam Liccardo (D–CA), the bill aims to make everyday payments faster, cheaper, and more reliable by modernizing access to core payment infrastructure while establishing consumer protection and federal supervisory standards for participating firms. Media coverage and sponsor statements place particular emphasis on potential benefits for fintech and digital-asset payment companies that currently rely on bank intermediaries to connect to Federal Reserve systems. [1] [2]

Overview

The PACE Act would open a statutory pathway for “qualified payment companies”—nonbank payment providers that meet defined standards—to obtain direct access to a subset of Federal Reserve payment rails. The bill’s core objectives are to lower consumer costs (for example, by reducing fees and intermediary spreads), speed up settlement for everyday transactions, and enhance reliability and competition in the U.S. payments ecosystem. Coverage identifies Fedwire, FedNow, and FedACH as the principal services contemplated for access, subject to risk controls and oversight. The proposal also includes prudential safeguards such as a full-reserve requirement for customer funds, segregation of customer assets, and risk-management and recordkeeping standards. [1] [2]

News reporting describes the bill as 23 pages in length and introduced with bipartisan backing as part of broader debates over the role of nonbank and digital-asset firms in U.S. payment networks. Supporters argue that permitting vetted, well-supervised nonbanks to access certain Federal Reserve services can reduce settlement friction and costs borne by consumers and small businesses. [1]

Background and Context

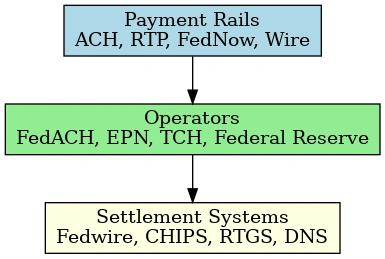

In the United States, access to core Federal Reserve payment systems—such as Fedwire for high-value settlement, FedNow for instant payments, and FedACH for automated clearinghouse transactions—has historically been limited to depository institutions. Nonbank payment providers typically access these rails indirectly by partnering with banks, a structure that can introduce delays, additional costs, and operational dependencies. The PACE Act responds to longstanding calls from parts of the fintech sector for more direct, regulated pathways to the Federal Reserve’s services. [1]

Media coverage of the bill situates it within parallel policy discussions about “skinny master accounts,” a concept that contemplates constrained forms of Federal Reserve account access for nonbank entities under strict limitations. Reporting indicates that the PACE Act acknowledges this concept and preserves final decision-making authority for the Federal Reserve Board over such account applications. This framing reflects active debate over how to balance innovation and competition with safeguards for operational integrity and financial stability. [3] [1]

Legislative History

The PACE Act was introduced in the U.S. House of Representatives on April 21, 2026, by Representatives Young Kim and Sam Liccardo. On the day of introduction, both the sponsors and multiple industry groups issued public statements of support, and several media outlets published analyses describing the bill’s objectives and potential implications. As of introduction, the bill’s number, committee referrals, and subsequent procedural steps were not publicly detailed in the materials cited here. [2] [3]

Purpose and Policy Goals

The sponsors frame the PACE Act as a consumer

- and competition-focused modernization of the U.S. payments system. By enabling direct access to designated Federal Reserve services for qualified nonbanks under a uniform federal framework, the bill aims to:

- Shorten settlement times for everyday payments.

- Lower or eliminate intermediary fees and processing costs that are often passed on to consumers.

- Enhance reliability and resilience by reducing dependence on multiple third-party links.

- Encourage competition and innovation among payment providers, including digital-asset and fintech firms that meet rigorous standards.

In sponsor materials, Rep. Young Kim states that the bill is intended to fix “outdated payment infrastructure” so Americans do not have to wait days or pay extra to move their own money. Supporters from industry associations similarly describe the proposal as a responsible route to faster and less expensive payments, contingent on strong oversight and consumer protections. [2] [1]

Key Provisions

Direct Access to Specified Federal Reserve Services

The PACE Act would establish a pathway for qualified nonbank payment providers to access certain Federal Reserve payment systems. Reporting identifies three principal services:

- Fedwire: The high-value funds-transfer service used for real-time gross settlement.

- FedNow: The instant payment service designed to facilitate 24/7/365 real-time payments.

- FedACH: The Federal Reserve’s automated clearinghouse processing service.

This access would be conditioned on qualification and ongoing compliance, with the Federal Reserve maintaining its usual risk controls and operational oversight as applicable. [1]

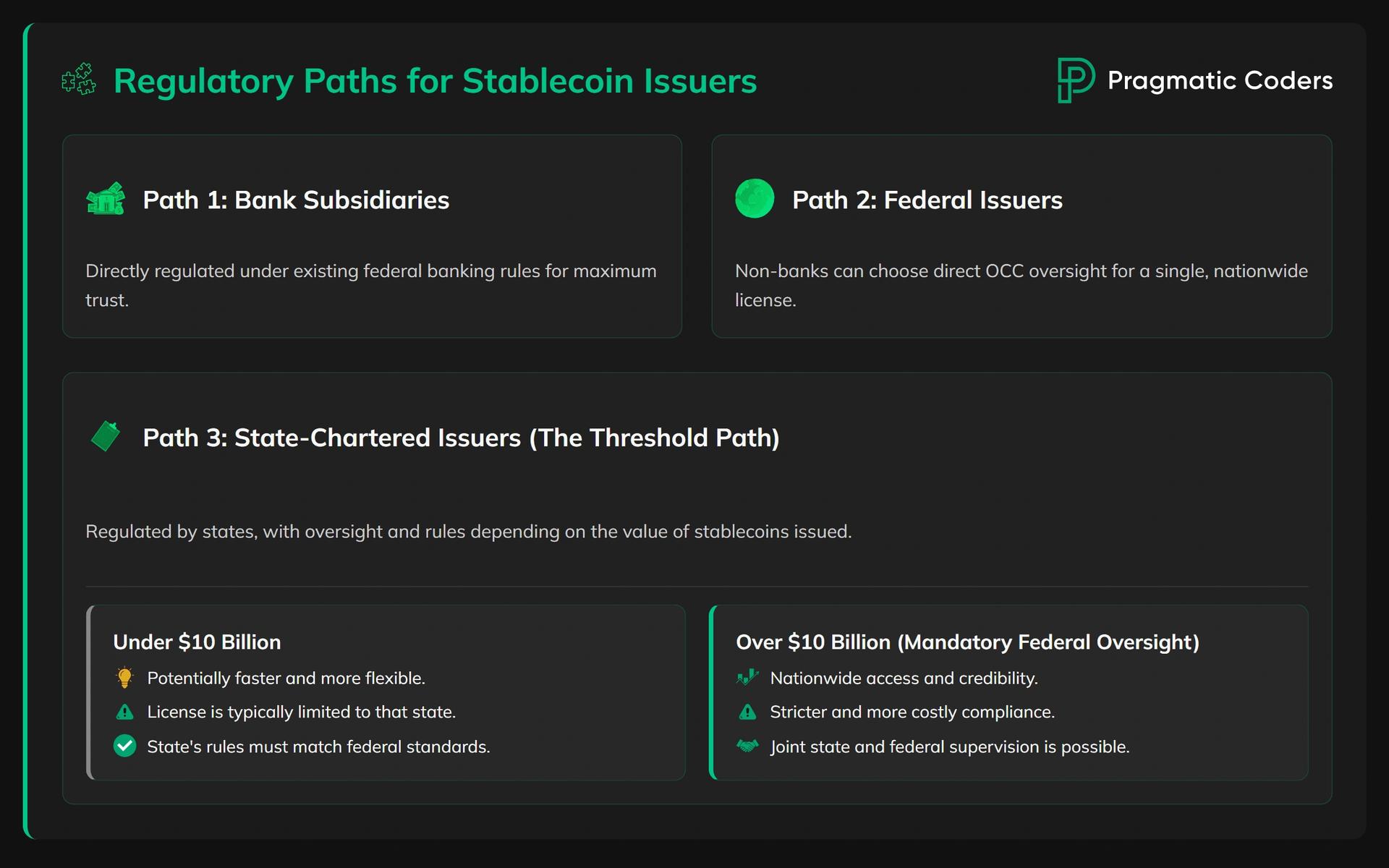

Optional Federal Supervisory Framework

The proposal contemplates an optional federal supervisory regime for eligible nonbank payment companies administered by the Office of the Comptroller of the Currency (OCC). Under this model, companies opting in would be held to federal standards for safety, soundness, consumer protection, and operational risk management as a condition of access. The OCC’s role would include examination and enforcement consistent with the framework created by the statute, in coordination with applicable Federal Reserve requirements tied to account or service access. [1]

Streamlined Federal Registration and Review Deadlines

The PACE Act envisions a federal registration process for qualified payment companies featuring clear standards and government review timelines. Sponsors characterize this as a means to reduce duplicative or protracted approvals across jurisdictions, especially for large multi-state payment firms that already hold numerous state licenses. By regularizing the process at the federal level, the bill seeks to create a more predictable on-ramp to Fed services for entities that meet the statutory and supervisory criteria. [2]

Full-Reserve and Segregation Requirements

To mitigate customer-fund risk, the bill would require participating payment firms to maintain 1:1 reserves for customer balances and to segregate those funds from company assets. These provisions are designed to minimize the risk that consumer funds are commingled or rehypothecated, and to simplify customer recovery in the event of a firm’s failure. [1] [2]

Insolvency and Consumer Priority

Sponsor materials describe consumer-first protections in failure scenarios, including prioritization of consumer claims over other creditors. Combined with full-reserve and segregation requirements, these measures are intended to enhance consumer recourse and reduce loss severity if a registered payment company becomes insolvent. [2]

Risk-Management and Recordkeeping Standards

Participating companies would need to demonstrate and maintain robust risk-management frameworks, compliance controls, and recordkeeping practices consistent with federal supervisory expectations. These standards are framed as prerequisites for access and as ongoing obligations subject to examination. [1]

Eligibility and “Qualified Payment Companies”

The PACE Act targets nonbank payment providers that offer money transmission or similar services but are not depository institutions. Reporting indicates that a practical benchmark for eligibility may include holding a substantial number of state money-transmitter licenses. Sponsor materials specifically reference a threshold of 40 or more state licenses as a criterion for electing into the federal framework under OCC supervision. The exact statutory definition of a “qualified payment company,” along with any asset, volume, operational, or compliance thresholds, would be detailed in the bill text and subsequent regulatory guidance. [1] [2]

Account Structure and “Skinny Master Accounts”

Coverage notes that the bill acknowledges the concept of “skinny master accounts”—a constrained form of Federal Reserve account access—and clarifies that the Federal Reserve Board retains final authority over applications for such access. The intent is to provide a standardized but carefully controlled mechanism for nonbank entities to interface with the Federal Reserve’s services, subject to the Fed’s risk criteria and discretion. The exact account architecture and operational parameters would depend on both statutory language and the Federal Reserve’s implementation policies. [3] [1]

Relationship to Digital-Asset Payment Firms

Media analyses highlight the PACE Act’s potential implications for regulated digital-asset payment companies, including stablecoin-focused firms, that could seek direct access to Federal Reserve services if they meet the qualification standards. Outlets specifically referenced U.S.-based companies such as Ripple and Circle as potential beneficiaries under the bill’s framework, while underscoring that eligibility would depend on statutory criteria and supervisory approvals. This reflects a broader trend of integrating blockchain-enabled payment solutions into mainstream payment pathways, contingent on regulatory oversight and consumer protections. [3] [1]

Some coverage also noted that at the time of reporting, a crypto-affiliated institution had been identified in media as having a form of access to Federal Reserve rails, illustrating both the demand for access pathways and the sensitivity of such arrangements. This context underscores why the PACE Act pairs potential access with full-reserve, segregation, and supervisory requirements. [3]

Support and Endorsements

The bill drew public endorsements from several trade associations and industry groups upon introduction. Organizations praising the proposal included:

- Financial Technology Association

- Blockchain Association

- The Digital Chamber

- Crypto Council for Innovation

In public statements, these groups emphasized competition, consumer benefits, and responsible modernization of payments infrastructure. For example, supporters described the bill as an “important step forward” for enabling qualified nonbank providers to deliver faster and more cost-effective payment services while operating under strong oversight. [2] [1]

Opposition and Concerns

While introductory materials emphasized bipartisan support and industry endorsements, media reporting also referenced opposition from segments of the banking industry. Critics have raised concerns about operational risk, the potential for fraud, and broader financial-stability implications of granting nonbank and crypto-affiliated firms access to Federal Reserve services. A statement attributed to the Colorado Bankers Association warned that “skinny master accounts” could create an “expedited fraud” channel if not carefully controlled. These concerns suggest that debate around the PACE Act would likely focus on the robustness of supervisory standards and the operational safeguards governing nonbank access. [3]

More generally, open questions include how the PACE framework would interact with existing state money-transmitter laws, how responsibilities would be divided among the Federal Reserve, OCC, and other federal and state regulators, and how to calibrate risk controls for nonbank participants using real-time and high-value settlement systems. These issues are typically central to policy deliberations about opening central banking services to a broader range of entities. [1]

Implementation Mechanics

Under the PACE framework as described, implementation would involve several coordinated steps:

- Federal registration under defined standards, with explicit review timelines to provide predictability for applicants.

- OCC-administered supervision for companies that opt into the federal framework, including examinations and enforcement consistent with prudential and consumer-protection aims.

- Federal Reserve evaluation of applications for account access, including the possibility of “skinny master accounts,” with the Fed Board retaining final authority over approvals and risk parameters.

- Ongoing compliance with full-reserve, segregation, and risk-management requirements, along with recordkeeping sufficient to support audits, examinations, and consumer recourse.

The specifics of each element—such as the volume thresholds, types of permissible activities, and exact services covered—would be clarified in the bill text and subsequent regulatory guidance and rulemaking. [2] [3]

Consumer Protections

The bill’s consumer-protection architecture centers on:

- Full reserve backing for customer funds at a 1:1 ratio.

- Segregation of these funds from company assets to prevent commingling.

- Restrictions on reuse of consumer funds that could elevate loss risk.

- Priority for consumers to recover funds if a provider fails.

Proponents argue these measures, combined with federal supervision, materially reduce consumer harm risks traditionally cited in opposition to nonbank access. Enforcement would rely on examination authority and clear standards for recordkeeping and disclosures to support audits and consumer claims. [2] [1]

See something wrong?

Average Rating

No ratings yet, be the first to rate!

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On June 18, 2026. 14:23 UTC

Edit summary:

Updated summary to note PACE Act Fed rails access and replaced id