0% read

Last updated:

Non-USD Stablecoins

Non-USD Stablecoins are a class of cryptocurrencies designed to maintain a stable value by being pegged to a fiat currency other than the United States dollar (USD). While the stablecoin market is heavily dominated by USD-pegged assets, a growing ecosystem of stablecoins pegged to currencies such as the Euro (EUR), Korean Won (KRW), Japanese Yen (JPY), Brazilian Real (BRL), and Singapore Dollar (SGD) is emerging to serve regional markets and specific financial use cases. [2]

Overview and Market Landscape

Non-USD stablecoins represent a small but developing segment of the broader cryptocurrency market. As of June 2023, this category accounted for less than 0.7% (under $1 billion) of the total fiat-linked stablecoin market capitalization of over $130 billion, with USD-pegged stablecoins comprising over 99.3%. [8] This dominance was reinforced by a July 2024 report from the Financial Stability Board, which noted that over 99.3% of fiat-pegged stablecoin supply on Ethereum was pegged to the USD. [6] This disparity continued into 2025, when the market capitalization of non-USD stablecoins was estimated to be under $500 million, compared to over $225 billion for their USD-pegged counterparts. Other analyses from the same period place the non-USD market share between 1-5% of the total stablecoin market. [2] [1] [5] [11]

Despite their smaller market share, these assets exhibit significant transaction activity that underscores the broader importance of stablecoins in the digital economy. As of late 2024, stablecoins accounted for over two-thirds of the total transaction volume in the cryptocurrency market. [12] By the end of 2025, the Polygon network alone had processed over $11.1 billion in lifetime transfer volume for non-USD stablecoins, representing over 43% of the total volume across major blockchains. This highlights their growing use in specific applications like payments and remittances, even as their total market cap remains a fraction of USD-pegged coins. [3]

Stablecoins pegged to over 15 different national currencies have been issued across Europe, Asia, Africa, and Latin America. The Euro (EUR) is the most prominent currency in this sector, a position bolstered by the regulatory clarity provided by Europe's Markets in Crypto-Assets (MiCA) regulation. This framework has fostered trust and encouraged the issuance of regulated stablecoins, such as Circle's EUROC. Adoption patterns are often regional, driven by local fintech partnerships and specific market demands, such as the need for BRL-denominated assets in Brazil's active crypto economy. [2] [1]

Types and Mechanisms

Non-USD stablecoins, like their USD-pegged counterparts, are categorized based on their underlying collateral and stabilization mechanism. The chosen model has significant implications for their stability, transparency, and regulatory treatment. [13] [14]

Fiat-Collateralized Stablecoins

This is the most common and widely trusted model, particularly in the regulated non-USD space. These stablecoins are pegged 1:1 to a specific fiat currency and are backed by reserves of that currency or equivalent assets like cash and short-term government securities. The reserves are held by a central issuing entity, which can be audited to verify that the tokens are fully backed. This model's stability and simplicity make it suitable for regulated environments like the European Union under MiCA. [12] [13]

Commodity-Collateralized Stablecoins

These stablecoins are backed by physical assets, most commonly precious metals like gold. Each token represents ownership of a specific quantity of the underlying commodity, which is stored in a secure, audited vault. While not pegged to a fiat currency, they are considered a type of non-USD stable asset because their value is tied to a globally recognized commodity rather than the U.S. dollar. The most prominent examples are PAX Gold (PAXG), pegged to the value of one troy ounce of gold, and Tether's XAU₮, a tokenized gold asset built on an omnichain framework for cross-chain transfers. [12] [13] [10] [15]

Crypto-Collateralized Stablecoins

These stablecoins are backed by a basket of other cryptocurrencies. To mitigate the price volatility of the underlying crypto collateral, these systems are typically over-collateralized, meaning the value of the deposited crypto assets is significantly higher than the value of the stablecoins issued. Their collateral is verifiable on-chain, offering a higher degree of transparency. The most well-known example of this mechanism is Dai (DAI), though it is pegged to the USD. This model is less prevalent in the non-USD space, which has so far prioritized the regulatory certainty of fiat-backed designs. [12] [13]

Algorithmic and Hybrid Stablecoins

Algorithmic stablecoins aim to maintain their peg through algorithms and smart contracts that automatically adjust the token supply in response to market demand, without relying on direct collateral. Hybrid models, such as Frax (FRAX), combine collateral with algorithmic adjustments. This category is considered highly experimental and carries significant risk, as demonstrated by the collapse of TerraUSD (UST) in May 2022, an event that wiped out billions in value and triggered a market-wide contraction. Due to these risks, this model is not widely used for non-USD stablecoins, especially as global regulators prioritize stability and consumer protection. [12] [13] [14]

Use Cases and Demand Drivers

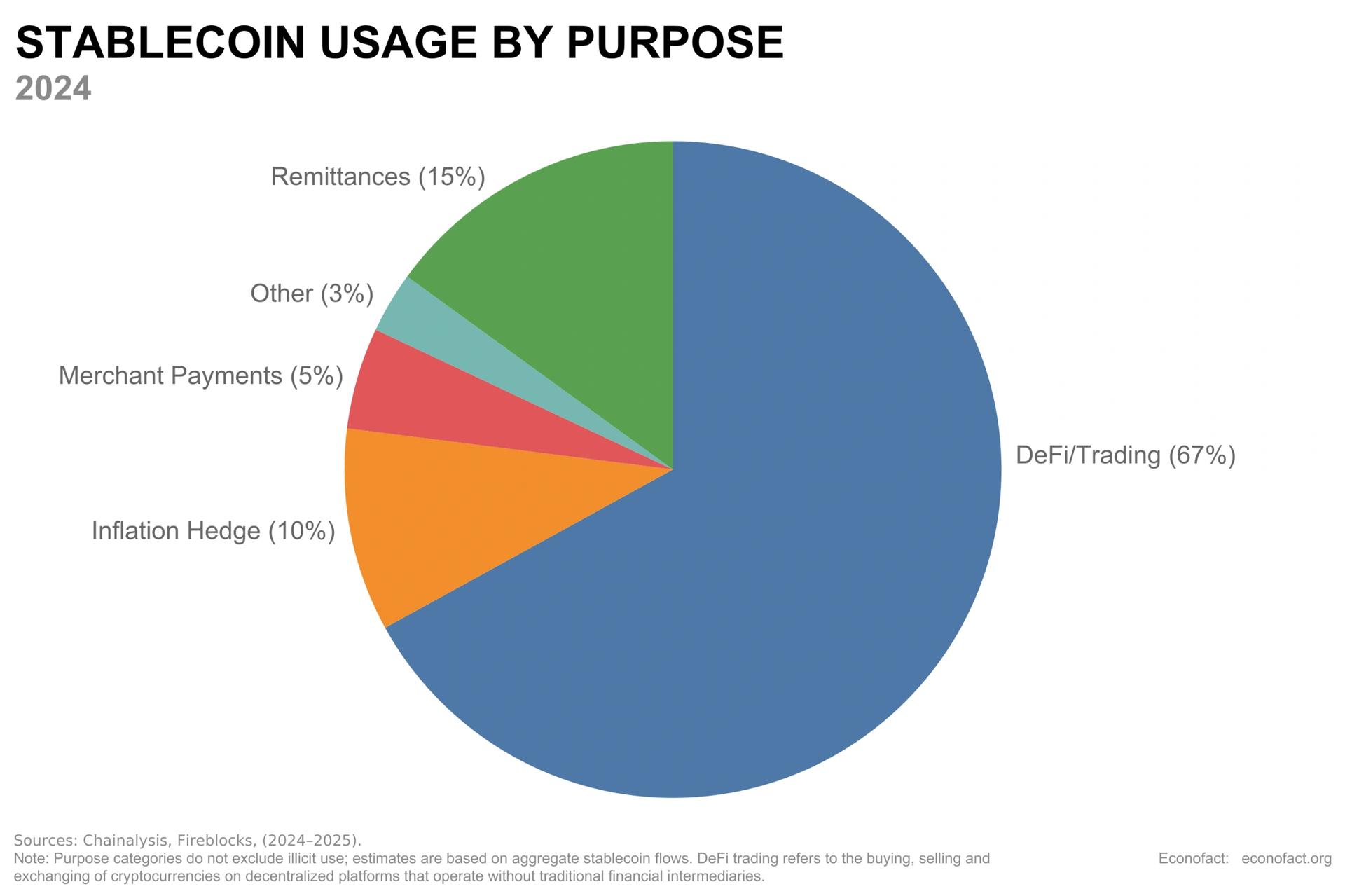

The growth of non-USD stablecoins is fueled by their ability to apply the core benefits of blockchain technology—such as 24/7 instant settlement, lower transaction costs, programmability, and borderless transfers—to local currencies. This unlocks several key use cases that are distinct from those served by USD-pegged assets. [2]

On-Chain Foreign Exchange (FX)

Non-USD stablecoins are instrumental in creating decentralized, always-on foreign exchange markets. They enable 24/7, near-instantaneous, and low-cost FX trading with atomic settlement on-chain, a significant improvement over traditional FX markets that operate on limited schedules and are highly fragmented. On-chain FX trading is often inefficient, as most non-USD currency pairs (e.g., EUR/JPY) must be routed through a USD stablecoin, involving two separate transactions and higher costs. The creation of direct liquidity pools for non-USD stablecoin pairs would enable more efficient, cheaper, and direct on-chain FX trading, democratizing access to these markets. [8] This is particularly valuable for currency pairs involving currencies not covered by the traditional Continuous Linked Settlement (CLS) system, which only supports 18 major world currencies. The increasing trading volume in pairs like EURC/USDC on both centralized and decentralized exchanges highlights the demand for this use case. [1] [2]

Remittances and Cross-Border Payments

These stablecoins offer a more efficient channel for the global remittance market, valued at over $800 billion. Traditional remittance services can be slow and costly, with average transaction costs of approximately 6%. Using USD-pegged stablecoins for non-USD remittances often forces the recipient to perform a second conversion, incurring foreign exchange risk and additional fees. By using a stablecoin native to the recipient's local currency, this intermediate step is eliminated, making the process faster, cheaper, and more direct. For example, analysis from the first quarter of 2024 showed that a $200 remittance from Sub-Saharan Africa was approximately 60% cheaper using stablecoins compared to traditional methods. [8] [12] This has the potential to reduce transaction fees from percentage points down to basis points. A key challenge to this use case is the development of "last-mile" infrastructure, which includes easy and efficient on

- and off-ramps between the local stablecoin and the local fiat currency. [8] In late 2025, African payments technology company Flutterwave selected Polygon as its default blockchain for cross-border payments, demonstrating the real-world application of this use case. [1] [2] [3]

Regional DeFi and Hedging

For individuals and businesses outside the United States, non-USD stablecoins provide a way to participate in the global crypto economy without taking on unwanted exchange rate risk against the U.S. dollar. By holding a stablecoin pegged to their local currency, they can hedge against USD volatility. Furthermore, the availability of stable assets in local currencies enables the development of regional Decentralized Finance (DeFi) ecosystems, including lending, borrowing, and yield-generating products denominated in currencies like EUR or JPY. [1]

Domestic Payment Infrastructure

In countries that lack efficient, real-time domestic payment systems (such as India's UPI or Brazil's PIX), stablecoins pegged to the local currency can serve as a modern, mobile-native, and programmable payment rail. They provide an alternative to physical cash and inefficient traditional banking systems, facilitating e-commerce and local peer-to-peer payments. For merchants and consumers outside the U.S., using USD-pegged stablecoins for daily commerce introduces exchange rate volatility risk. Non-USD stablecoins provide a stable unit of account in the local currency, eliminating this risk and making digital assets a more practical medium of exchange for everyday transactions. [8] The expansion of companies like DeCard, which uses Polygon to enable stablecoin payments for merchants, and Shift4, which is bringing 24/7 stablecoin settlement to global commerce, points to the growing adoption of this model. [2] [3]

Types by Pegged Currency

The non-USD stablecoin ecosystem is diverse, with projects targeting a wide range of currencies and regions. The Euro is the most developed currency in this market, but a growing number of stablecoins have been launched for other major and emerging market currencies.

Euro-Pegged Stablecoins

The Euro is the most developed non-USD stablecoin market, benefiting from the large European economy and the clear regulatory environment established by the Markets in Crypto-Assets (MiCA) regulation. These projects include:

- Circle EUROC (EURC): A fully-reserved, Euro-backed stablecoin issued by Circle, the company behind USDC. It operates under an E-Money Token (EMT) license within Europe's MiCA framework, giving it a strong regulatory foundation. It has also been approved by the Dubai International Financial Centre (DIFC) as a recognized crypto token. [9]

- Stasis EURO (EURS): One of the earliest Euro-pegged stablecoins, backed by reserves held in partner financial institutions.

- Tether EURt (EURT): A Euro-pegged stablecoin from Tether, the issuer of the market-leading USDT stablecoin.

- Other Issuers: Financial institutions like Societe Generale and regulated firms such as Monerium have also issued Euro-pegged stablecoins. [1] [2]

Korean Won (KRW) Stablecoins

Stablecoins pegged to the South Korean won (KRW) emerged to serve global DeFi markets, with interest in the sector growing after South Korea's central bank suspended its retail CBDC pilot in 2025, creating an opening for private issuers. [9]

KRWQ

Launched in late 2025, KRWQ is a fiat-backed stablecoin pegged 1:1 to the Korean Won. It was developed by IQ in partnership with Frax and was the first KRW stablecoin to launch on the Base network. The asset is designed for interoperability, using LayerZero's Omnichain Fungible Token (OFT) standard. Within a month of its launch, in November 2025, KRWQ surpassed ₩1 billion in trading volume. [17] [18]

British Pound (GBP) Stablecoins

The market for British Pound-pegged stablecoins includes projects such as GBPA. In April 2025, J.P. Morgan also added support for the British Pound to its blockchain-based payment service, Kinexys, signaling growing institutional interest in tokenized sterling.

Japanese Yen (JPY) Stablecoins

Several stablecoins are pegged to the Japanese Yen. Notable projects include GYEN (from GMO) and JPYC. As of May 2024, GYEN had a market capitalization of approximately $14 million. [6] The ecosystem is also seeing interest from traditional finance, with Japan's second-largest bank, Sumitomo Mitsui Banking Corporation (SMBC), exploring the launch of a stablecoin. Major crypto firms like Circle are also seeking regulatory approval (as of August 2025) to launch JPY-pegged stablecoins in the country. [9]

Singapore Dollar (SGD) Stablecoins

The Singapore Dollar stablecoin space is led by XSGD, issued by the fintech firm StraitsX. As a licensed Major Payment Institution by the Monetary Authority of Singapore (MAS), XSGD is a regulated stablecoin that serves the Southeast Asian market. As of September 2023, its market capitalization was over $30 million. [16]

Latin American Stablecoins

- Brazilian Real (BRL): Brazil has one of the most active non-USD stablecoin markets, featuring multiple projects like BRZ, BRLA, and BRL1. The Brazilian Digital Token (BRZ) is one of the largest non-USD, non-EUR stablecoins, with a market capitalization of $195 million as of May 2024. [6]

- Mexican Peso (MXN): The Mexican market includes stablecoins such as MXNe and MXNB.

- Colombian Peso (COP): COPM is a stablecoin pegged to the Colombian Peso.

African Stablecoins

- Nigerian Naira (NGN): Stablecoins such as cNGN and NGNC have been launched to serve Africa's largest economy.

- Kenyan Shilling (KES): cKES is a stablecoin pegged to the Kenyan Shilling.

Other G10 Currency Stablecoins

- Canadian Dollar (CAD): The Canadian market has projects like CADC.

- Australian Dollar (AUD): AUDF is a stablecoin pegged to the Australian Dollar.

Other Stablecoins

- Chinese Yuan (Offshore) (CNH): Stablecoins pegged to the offshore yuan, such as CNHC and Tether's omnichain CNHT0, primarily focus on cross-border trade and remittances. [10]

- Turkish Lira (TRY): TRYB, issued by BiLira, is a major stablecoin in the Turkish market. As of May 2024, it had a market capitalization of $36 million. [6]

- Indonesian Rupiah (IDR): Projects like IDRX have been launched to serve the Indonesian market.

- Emirati Dirham (AED): Tether issues a stablecoin backed by the Emirati Dirham. [12]

Challenges to Adoption

Despite their potential, non-USD stablecoins face significant hurdles in gaining widespread adoption and competing with the dominance of their USD-pegged counterparts.

Primacy of the U.S. Dollar

The U.S. dollar's role as the world's primary reserve currency is the single largest challenge. The USD is used in approximately 80% of global trade invoicing and is on one side of nearly 90% of all FX trades. In the crypto world, this translates into a primary demand for efficient on-chain access to the U.S. dollar. For many users globally, USD-pegged stablecoins serve as a safe-haven asset and a gateway to the deepest pools of liquidity in crypto trading and DeFi. Aymeric Salley, a co-founder of stablecoin issuer StraitsX, argued in 2021 that this dominance stemmed not just from demand for the dollar itself, but from a "lack of trusted and compliant alternatives" in other currencies. Overcoming this powerful network effect remains a monumental task. [1] [2] [4]

Price Stability and De-Peg Risk

While named for stability, research indicates that no stablecoin has been able to perfectly maintain its peg at all times. Analysis from the Bank for International Settlements (BIS) in late 2023 concluded that even the largest, most liquid fiat-backed stablecoins experience periods of price deviation, creating "run risk" and undermining their use as a reliable means of payment. [14] [11]

Specifically, the BIS found that large intraday price swings can occur, with Tether (USDT) having experienced a deviation as high as 13% below its peg. While such events were rare, the constant potential for de-pegging—highlighted by the SVB-induced run on USDC in March 2023 and the total collapse of the algorithmic TerraUSD in 2022—remains a fundamental challenge to user trust. The same research noted that fiat-backed stablecoins pegged to the Euro (EUR) have demonstrated an ability to track their peg closely, a performance level comparable to that of USD-pegged stablecoins. In contrast, stablecoins pegged to currencies such as the Indonesian Rupiah (IDR), Singapore Dollar (SGD), and Turkish Lira (TRY) have experienced larger deviations, potentially due to the higher volatility of their underlying reserve assets. [14] The BIS also critiqued stablecoins for failing key tests of money, such as "singleness" (always trading at par), "elasticity" (flexible supply), and "integrity" (resistance to illicit use), further complicating their path to mainstream adoption as a true cash alternative. [11]

Liquidity and Infrastructure

The non-USD stablecoin market suffers from liquidity fragmentation. The market is split across many different currencies, each with relatively low supply and trading volume compared to giants like USDT and USDC. This "liquidity trap" makes them less attractive for large-scale trading and DeFi protocols, which require deep liquidity to function efficiently. The development of robust "last-mile" on

- and off-ramps through partnerships with local banks and payment processors is considered a significant hurdle. The work of issuers like StraitsX in partnering with local payment providers in Singapore is an example of the infrastructure required for mainstream adoption. [8] Furthermore, mainstream adoption requires native support from wallets, custodians, on/off-ramps, and oracle services, which remains limited for most non-USD tokens. A better user experience (UX) for holding and swapping multiple currencies within digital wallets is also needed. [1] [2]

Regulatory Complexity and CBDC Competition

Navigating varied and complex legal landscapes is a primary challenge. While frameworks like MiCA in Europe, rules from Japan's Financial Services Agency (FSA), and Singapore's Payment Services Act provide regulatory clarity, many other jurisdictions have unclear or restrictive policies. [4] Beyond regulatory hurdles, gaining user trust is crucial. Issuers must demonstrate that their assets are fully backed by high-quality, liquid reserves, reinforcing this commitment with regular, transparent audits. [8]

While a small fraction of total activity (estimated at less than 1% by Chainalysis), the use of stablecoins in illicit activities like fraud and sanctions evasion poses a reputational and regulatory risk. In response, centralized issuers like Circle and Tether collaborate with law enforcement and have the technical ability to freeze or burn tokens in wallets linked to illicit activity. This contrasts with decentralized stablecoins like Dai, which are managed by autonomous smart contracts and are designed to be censorship-resistant. [12]

Additionally, the relationship with Central Bank Digital Currencies (CBDCs) is complex and evolving. While a government-issued digital currency could compete with private stablecoins, by 2025 a trend emerged where several major economies began to de-prioritize or halt their retail CBDC projects, creating a potential opening for regulated private issuers. [9]

- In the United States, the House of Representatives passed the Anti-CBDC Surveillance State Act in July 2025, and the Federal Reserve Chair committed to not issuing a retail CBDC, citing concerns over government surveillance. [9]

- The United Kingdom's Bank of England shifted its focus in mid-2025 from a retail CBDC to supporting private sector tokenized deposit projects. [9]

- South Korea's central bank suspended its retail CBDC pilot in late 2025, reportedly due to resistance from commercial banks and a new legislative push to lower entry barriers for private stablecoin issuers. [9]

This trend contrasts with China, which continues to advance its e-CNY project to increase state monetary control. Meanwhile, the European Union continues its multi-year "preparation phase" for a potential digital euro. This retreat by some central banks from the retail digital currency space has been viewed as an opportunity by stablecoin issuers like Circle and Tether, who increased their engagement in markets like South Korea and Japan in 2025. [9]

Recent Developments and Future Outlook

Analysts project significant growth potential for the non-USD stablecoin sector, viewing it as a "growing corner of the crypto ecosystem" with a "clear product-market fit." [8] J.P. Morgan Global Research projected in late 2025 that the overall stablecoin market could grow from ~500 billion and $750 billion in the coming years. [11] Growth in the non-USD segment is expected to be driven by dominance in niche markets, such as Euro-zone DeFi and Latin American remittances, rather than a direct global challenge to USD stablecoins. Geopolitical trends involving de-dollarization in traditional finance could also accelerate the search for non-USD alternatives in the digital asset space. [1]

Initiatives in late 2025 and early 2026 signaled growing momentum:

- Growing Hub on Polygon: By the end of 2025, Polygon PoS emerged as a leading network for non-USD stablecoins, processing over $11.1 billion in lifetime volume. This growth was supported by technical upgrades like the Madhugiri hardfork, which increased network throughput specifically to support payment applications. [3]

- Expansion of Omnichain Non-USD Assets: In January 2026, Tether's omnichain framework (USDT0) was expanded to support non-USD assets, including tokenized gold (XAUT0) and offshore yuan (CNHT0). The Conflux network became the first ecosystem to launch CNHt0 for cross-border commerce. [10]

- Expansion in Asian Markets: 2025 was a pivotal year for the Asian stablecoin market, driven by increasing regulatory clarity in key financial hubs like Hong Kong, Japan, and Singapore. This clearer framework attracted traditional finance (TradFi) institutions, including Grab, Nomura, and Mitsubishi UFJ, with a strong market preference for secure, fiat-backed models. This trend was highlighted by the success of new assets like the Korean Won-pegged KRWQ, which surpassed ₩1 billion in trading volume shortly after its launch in late 2025. Alex Lim of the Asia Stablecoin Alliance noted this milestone "underscores the growing global interest in KRW stablecoins," while Frax founder Sam Kazemian highlighted how such projects show "new fiat-backed stablecoins can integrate seamlessly with global DeFi liquidity." In addition to new entrants, established crypto firms like Coinbase, Circle, and Tether also explored expansion in the region. [17] [18] [9]

- Payment Provider Integrations: In late 2025, several major payment and fintech firms announced integrations leveraging Polygon for stablecoin payments, including Flutterwave (cross-border), Revolut, DeCard, and Shift4. In November 2025, Mastercard also selected the network to power verified username transfers for self-custody wallets. [3]

- J.P. Morgan added support for the British Pound (GBP) to its blockchain-based payment service, Kinexys, in April 2025.

- Sumitomo Mitsui Banking Corporation (SMBC), Japan's second-largest bank, began exploring the launch of a stablecoin in partnership with Ava Labs.

- In January 2026, Polygon Labs announced its intent to acquire fintech firms Coinme and Sequence to expand its suite of regulated payment solutions in the United States. [3]

- In April 2025, a Russian finance ministry official publicly stated that the country should develop its own stablecoins.

This growing interest from both the crypto industry and traditional finance highlights the recognition of the potential for stablecoins pegged to local currencies. [2]

See something wrong?

Average Rating

Based on over 1 ratings

How was your experience?

Give this wiki a quick rating to let us know!

Edited By

On July 30, 2026. 17:50 UTC

Edit summary:

Expanded non-USD stablecoin summary